SBA Loans

Our experienced bankers are passionate about helping business owners and entrepreneurs structure the ideal financing solution that fuels their ambitions. Discover the Texas Capital difference.

SBA Loans

Our experienced bankers are passionate about helping business owners and entrepreneurs structure the ideal financing solution that fuels their ambitions. Discover the Texas Capital difference.

Top 5 SBA Lender in Texas

We're proud to rank among the U.S. Small Business Administration's top 5 SBA 7(a) lenders headquartered in Texas to empower Texas-based businesses with the capital and expertise they need to scale.

Top 5 SBA Lender in Texas

We're proud to rank among the U.S. Small Business Administration's top 5 SBA 7(a) lenders headquartered in Texas to empower Texas-based businesses with the capital and expertise they need to scale.

SBA Financing Built for Texas Businesses

As one of the top Preferred SBA lenders headquartered in Texas, we understand the unique challenges facing Texas business owners and entrepreneurs. Our fully dedicated, in-market SBA team of bankers, processors, and loan closers combine over 100 years of SBA lending experience with flexible financing solutions to meet your needs. Whether you’re looking to expand operations, enter a new market, acquire a competitor, or invest in critical assets, our team has the experience and resources to structure a financing solution that works for your business.

Dedicated SBA Experts

Experienced, in-market business bankers dedicated to SBA lending.

Preferred SBA Lender

As an SBA Preferred Lender, we expedite the approval process to deliver capital when you need it most.

Flexible Terms

Loan terms tailored specifically to match your unique business needs and goals.

Benefits of an SBA Loan

An SBA 7(a) or 504 Loan provides businesses with access to capital that might not otherwise be available, with more flexible underwriting than conventional business loans. The U.S. Small Business Administration partners with approved lenders, like Texas Capital, to reduce risk, allowing lenders to offer more favorable terms to small business owners and entrepreneurs who are working to grow, acquire, or strengthen their operations.

With an SBA Loan, businesses can benefit from:

- Lower down payment requirements

- Longer repayment terms — up to 25 years

- Lower cash flow requirements to cover payments

- Ability to conserve cash for operating expenses

SBA 7(a) Loan

The SBA 7(a) Loan Program is one of the most widely selected SBA loans due to its flexibility. Common uses include expanding or acquiring a business, partnership buy-ins or buy-outs, real estate purchase and refinance. Key benefits include:

- Loan amounts up to $5 million

- Lower down payment requirements

- Longer repayments up to 25 years

- Lower fixed or variable interest rates than traditional loans

All loans subject to Texas Capital credit approval and SBA eligibility.

SBA 504 Loan

The SBA 504 Loan Program is a powerful financing tool for businesses investing in land, buildings and large equipment. Unlike the 7(a) program, SBA 504 loans are structured with a Community Development Corporation (CDC) who works with Texas Capital to provide flexible financing for clients. Key benefits include:

- Loan amounts up to $15 million

- Up to 90% financing – with typically a 10% down payment

- Longer repayments up to 25 years

- Fixed or floating interest rates

All loans subject to Texas Capital credit approval and SBA eligibility.

Connect with our SBA Loan team.

Discover how an SBA Loan can fuel your business growth by starting a conversation with one of our SBA Loan specialists today.

Every member of the Texas Capital team has been great to work with — from the underwriters to my banking lender. The entire SBA team is extremely thorough and professional.

President and CEO

Physical Therapy & Wellness Center | Houston, TX

Case Studies

Case Studies

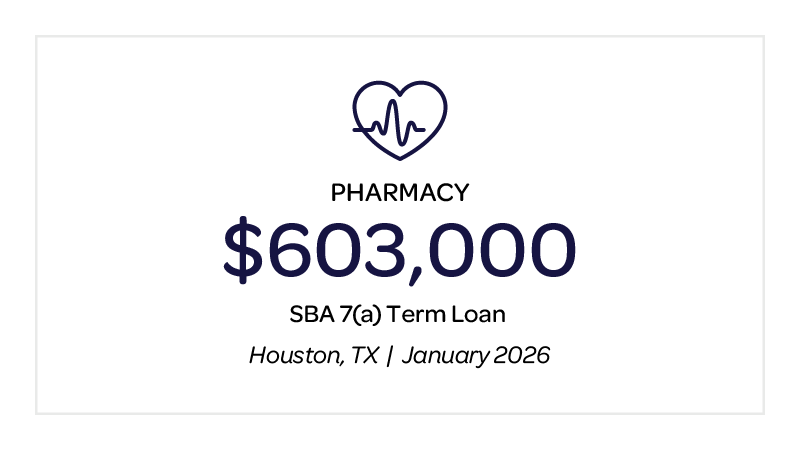

SBA 7(a) Financing for Pharmacy Expansion & Build-Out

<p>See how Texas Capital provided $603K in SBA 7(a) financing for a Houston pharmacy expansion, including clean room build-out and equipment.</p>

Case Studies

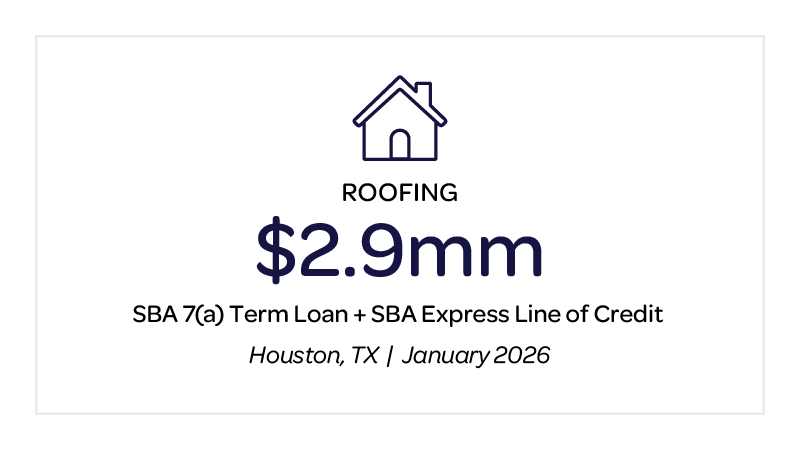

SBA 7(a) Acquisition Financing for Roofing Contractors

<p>Learn how Texas Capital financed a $2.9M acquisition for a Houston roofing contractor using an SBA 7(a) term loan and line of credit. </p>

Case Studies

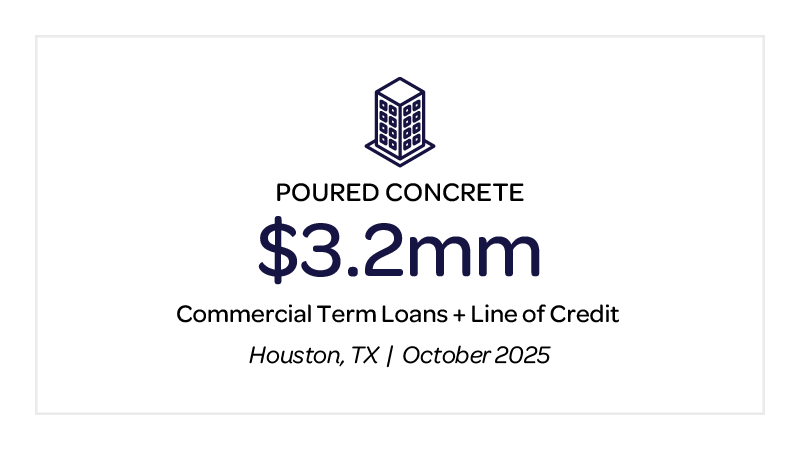

Business Acquisition Financing for Concrete Contractors

<p>Discover how Texas Capital structured $3.2M in acquisition financing for a Houston concrete contractor, combining term loans and real estate financing with fixed rates.</p>

Frequently Asked Questions

How do SBA Loans work?

The Small Business Administration (SBA) is a U.S. government agency that approves billions of dollars in loans to small businesses every year. Most SBA Loans are issued through a bank, a credit union or other lending institution, and the SBA guarantees part of the loan. This guarantee allows banks to utilize more flexible underwriting guidelines in evaluating an SBA Loan request, since a portion of the bank’s credit risk is offset by the government’s guarantee. The guarantee amount varies depending on the size and type of loan 50%-100%.

Interest rates on SBA Loans are set by the lender, in keeping with SBA guidelines. The rate is based on the prime rate, plus an additional markup rate called the spread. Interest rates vary slightly depending on the use of funds, collateral and terms of the loan.

What does it mean to be a Preferred SBA Lender?

Texas Capital Bank is a Preferred SBA Lender. SBA Loans require a high level of expertise to ensure a smooth application process, so you’ll want to select a lender who is a Preferred SBA Lender. This means the bank is authorized and approved to underwrite the credit application instead of submitting it to the SBA for approval, which will save time in completing the loan process. Preferred lenders are able to provide an approval 2-6 weeks faster than lenders who are not qualified as Preferred SBA Lenders.

What qualifies my business for an SBA Loan?

Not all business types are eligible for an SBA Loan. Financial institutions, life insurance providers, passive businesses (for example, investment properties) and speculative businesses (such as oil exploration) are among those who cannot secure SBA financing.

In addition, you must:

- Be a U.S. Citizen

- Do business in the U.S.

- Operate for profit

- Meet SBA business size standards

- Have a reasonable amount of invested equity

- Have a demonstrable ability to repay the loan

- Owners with 20% or more ownership must guarantee the loan

How can SBA loan funds be used?

This list is not all-inclusive, but some of the most common approved loan purposes are:

- Business acquisition and partner buyouts

- Purchase of owner-occupied commercial real estate, including special use properties

- Building construction or expansion

- Debt refinancing

- Purchase of machinery or equipment

- Purchase of furniture, fixtures and/or leasehold improvements

- Working capital

What information do I need to provide during this process?

Preliminary Discussion

- Overview of business and loan purpose

- Interim financial statements for the business

- Three years’ business tax returns and three years projected tax returns

- Personal financial statements and tax returns

- Joint returns with spouse

At Application

- Completed loan application

- Business plan with projections and assumptions

- Accounts payables and accounts receivables aging reports

- Affiliate company information

- Copy of purchase agreement (for business purchases, real estate and partner buyout)

- Owner’s and manager’s resume

During Loan Process

- Be ready to provide additional information during the loan process. Sometimes the documentation may not paint a full picture, and the loan officer may ask for your help in filling in any gaps.

What is the difference between an SBA Loan and a conventional Small Business Loan?

Both financing options can help fund your business, but they work differently. Here's how Texas Capital Bank's offerings compare:

Texas Capital SBA 7(a) Loans:

- Government Backing: The US Small Business Administration guarantees a portion of the loan, reducing lender risk

- Larger Loan Amounts: $500,000 to $5,000,000 available

- Longer Terms: 10 to 25 years depending on loan purpose

- Flexible Uses: Launch new products, fund growth, acquire companies, purchase real estate, equipment, or refinance existing debt

- Fixed or Variable Rates: You choose the rate structure that works for your business

- Expert Support: Texas Capital's lending team handles processing, packaging, and application

- Lower Down Payments: SBA backing allows more flexible equity requirements

- Broader Qualification: More accessible for businesses that might not qualify for conventional financing

Texas Capital Small Business Loans:

- Conventional Financing: Direct bank lending without government guarantee

- Smaller Loan Amounts: Up to $250,000

- Faster Processing: Quicker approval than SBA loans

- Simpler Application: Fewer requirements and documentation

- Qualification Requirements: 680+ credit score, minimum one year in business

- Flexible Terms: Customized to your business needs

- Immediate Availability: Ideal for smaller capital needs and quick funding

Bottom Line: If you need substantial capital ($500K+) for major growth, acquisitions, or real estate, Texas Capital's SBA 7(a) loans offer government-backed advantages with longer terms. For smaller needs ($15K-$250K) and faster turnaround, conventional small business loans are a solid choice.

Connect with our SBA Loan team.

Discover how an SBA Loan can fuel your business growth by starting a conversation with one of our SBA Loan specialists today.

Additional Insights

Commercial Banking

2026 ACH Rule Changes: What Business Owners Needs to Know

<p>Learn how 2026 ACH Rule Changes affect your business. Discover fraud monitoring requirements, payment description updates, and action steps needed before March 20 and June 19 deadlines.</p><p> </p>

Commercial Banking

How to Detect and Prevent Check Fraud in Business Banking

<p>Check Fraud is one of the oldest forms of financial crime, yet it continues to evolve and cost businesses billions each year. </p>

Commercial Banking

How to spot Social Engineering in Business Banking

<p>Social Engineering has become one of the most dangerous and deceptive threats to business banking.</p>