Your Report Card — Week of March 31, 2025

Essential Economics

— Mark Frears

What you can control

As we enter another week of great uncertainty, you must still set goals. There are five parts to every goal. First, it must be specific, not just “do better.” Second, it must be measurable: not just to lose weight, but how much. Third, it must be achievable, not impossible. Fourth, it will be realistic: I will not play in the NHL. Fifth, it must be timely: you will set a target date. In addition, it will help immensely to break up your big goals into smaller ones, and you should write it down (in ink) and keep it where you can see it. The most important thing is to get started.

One of the things that could impact your ability to reach a goal is your credit report. How are you doing?

Your credit report card?

How you manage your money is captured in your credit report. There are three companies that track your credit: Equifax, Experian and TransUnion. You can obtain a free credit report once a year from these three by going to annualcreditreport.com. I would encourage you to do this, even if you think you have great credit. There can be things that show up on the report that might not be totally accurate, and it would greatly benefit you to make sure only your activity is reflected. Identity theft is a huge issue that could affect anyone.

Details

Let’s look at the nuts and bolts of your report. The five inputs are presented below, and number one on the list is your payment history. As this is 35% of the report, it is vital that you pay your bills on time, and it is the best way to work on repairing a poor credit report.

- Payment History 35% (Are you paying on time?)

- Debt Usage 30% (Are you maxed out on your credit card, or paying it off monthly?)

- Age of your credit 15% (How long have you had a credit history?)

- Types of accounts 10% (Do you have a variety of debt, such as mortgage, car or credit card?)

- Application History 10% (Are you applying for a lot of credit?)

Your Credit Score is calculated from these five factors. Credit Scores, often sourced from Fair Isaac Company (FICO), generally range from 300 to 850. Anything over 700 is considered good, and over 760 is excellent. The free credit report website cited above does not give your credit score, but it can be obtained through other sources.

You may have another easier way to improve your score, as the Consumer Financial Protection Board (CFPB) has decided to remove tax-lien and civil-judgement data from credit reports. After this change was made, millions of consumers have seen an improvement in their credit score. If these types of problems were the primary issue with your report, you could have seen an increase of 40 points. If you have other issues with your credit, this will only help you a little.

Student loans

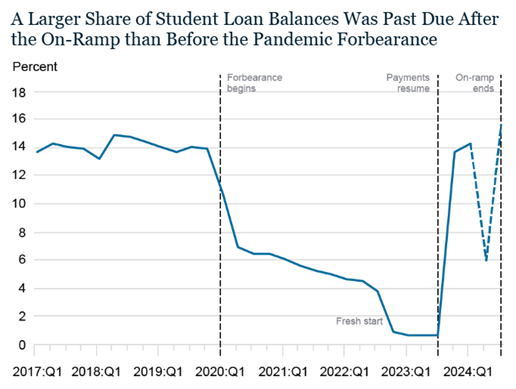

The pandemic forbearance had a material impact on consumers with student loans, especially those with a previous delinquency. They got an immediate bump in their credit score when these were temporarily erased. The time has come to pay the piper, as these payment histories will be restored in the first half of 2025. This will impact more than nine million student loan borrowers, per the New York Fed Consumer Credit Panel.

Borrowers were given an “on-ramp” period to get back on track, and that ended in September 2024. As you can see below, after the on-ramp, there will be a higher percentage of past due loans than before the pandemic.

Source: NY Fed Consumer Credit Panel/Equifax; Federal Student Aid

For consumers with credit scores over 760, a new delinquency could lower their score by 171 points, per the NY Fed.

Impact on other areas

Your credit report will not just affect you when applying for a car loan or mortgage. It will have an impact on the rate you pay on a loan, your cost of insurance (they now look over this report), and even employment. Employers have learned that how you manage your money is a good indicator of how you manage life.

Economic releases

Last week continued the story of ups and downs. Confidence lower, but Durables higher. GDP a bit higher and Personal Spending slower than expected.

This week’s calendar is focused on employment with JOLTS, ADP, Initial Jobless Claims and nonfarm payroll. See below for more detail.

Wrap-Up

Whether you are starting a home project, getting in shape, looking at your credit report or going through your emails, it is so important to take that first step. Get going!!

| Upcoming Economic Releases: | Period | Expected | Previous | |

|---|---|---|---|---|

| 31-Mar | MNI Chicago PMI | Mar | 45.0 | 45.5 |

| 31-Mar | Dallas Fed Manuf Activity | Mar | (5.0) | (8.3) |

| 1-Apr | Construction Spending MoM | Feb | 0.3% | -0.2% |

| 1-Apr | JOLTS Job Openings | Feb | 7,680,000 | 7,740,000 |

| 1-Apr | ISM Manufacturing Index | Mar | 49.5 | 50.3 |

| 1-Apr | ISM Manufacturing Prices Paid | Mar | 64.8 | 62.4 |

| 1-Apr | ISM Manufacturing Employment | Mar | N/A | 47.6 |

| 1-Apr | ISM Manufacturing New Orders | Mar | N/A | 48.6 |

| 1-Apr | Dallas Fed Services Activity | Mar | N/A | 4.6 |

| 1-Apr | Ward's Total Vehicle Sales | Mar | 16,050,000 | 16,000,000 |

| 2-Apr | ADP Employment Change | Mar | 120,000 | 77,000 |

| 2-Apr | Factory Orders | Feb | 0.5% | 1.7% |

| 2-Apr | Factory Orders ex Transportation | Feb | 0.4% | 0.2% |

| 3-Apr | Challenger Job cuts YoY | Mar | N/A | 103.2% |

| 3-Apr | Initial Jobless Claims | 29-Mar | 225,000 | 224,000 |

| 3-Apr | Continuing Claims | 22-Mar | 1,870,000 | 1,856,000 |

| 3-Apr | ISM Services Index | Mar | 53.0 | 53.5 |

| 3-Apr | ISM Services Prices Paid | Mar | N/A | 62.6 |

| 3-Apr | ISM Services Employment | Mar | N/A | 53.9 |

| 3-Apr | ISM Services New Orders | Mar | N/A | 52.2 |

| 4-Apr | Change in Nonfarm Payrolls | Mar | 135,000 | 151,000 |

| 4-Apr | Change in Private Payrolls | Mar | 130,000 | 140,000 |

| 4-Apr | Unemployment Rate | Mar | 4.1% | 4.1% |

| 4-Apr | Avg Hourly Earnings MoM | Mar | 0.3% | 0.3% |

| 4-Apr | Avg Hourly Earnings YoY | Mar | 3.9% | 4.0% |

| 4-Apr | Labor Force Participation Rate | Mar | 62.4% | 62.4% |

| 4-Apr | Underemployment Rate | Mar | N/A | 8.0% |

Mark Frears is a Senior Investment Advisor, Managing Director, at Texas Capital Bank Private Wealth Advisors. He holds a Bachelor of Science from The University of Washington, and an MBA from University of Texas – Dallas.

The contents of this article are subject to the terms and conditions available here.

Texas Capital Private Bank™ refers to the wealth management services offered by the bank and non-bank entities comprising the Texas Capital brand, including Texas Capital Bank Private Wealth Advisors (PWA). Nothing herein is intended to constitute an offer to sell or buy, or a solicitation of an offer to sell or buy securities.

Investing is subject to a high degree of investment risk, including the possible loss of the entire amount of an investment. You should carefully read and review all information provided by PWA, including PWA’s Form ADV, Part 2A brochure and all supplements thereto, before making an investment.

Neither PWA, the Bank nor any of their respective employees provides tax or legal advice. Nothing contained on this website (including any attachments) is intended as tax or legal advice for any recipient, nor should it be relied on as such. Taxpayers should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or legal counsel. The wealth strategy team at PWA can work with your attorney to facilitate the desired structure of your estate plan. The information contained on this website is not a complete summary or statement of all available data necessary for making an investment decision, and does not constitute a recommendation. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of the authors and not necessarily those of PWA or the Bank.

©2026 Texas Capital Bank Wealth Management Services, Inc., a wholly owned subsidiary of Texas Capital Bank. All rights reserved.

Texas Capital Bank Private Wealth Advisors and the Texas Capital Bank Private Wealth Advisors logo are trademarks of Texas Capital Bancshares, Inc., and Texas Capital Bank.

www.texascapitalbank.com NASDAQ®: TCBI